A Health Savings Account (HSA) is a tax-advantaged account designed to help individuals with high-deductible health plans save and pay for qualified medical expenses. To make the most of HSA benefits, you can use these accounts to save on health plan premiums, reduce your annual tax bill, stretch your spending power, and invest for long-term retirement savings.

HSAs continue to grow in popularity. There are more than 41 million HSAs - a growth rate of 6% for the year ending in 2025 - with nearly $174 billion in assets, according to research from Devenir.

Clearly, people recognize the value of HSAs and are finding ways to take advantage to improve their healthcare affordability.

HSAs bring the potential for tax savings, healthcare savings, retirement savings, and so much more.1 In fact, you can use tax-free money in your Health Savings Account to spend on qualified medical expenses, including thousands of items you use every day.

Now, let's jump in. This article counts 10 ways to make the most of an HSA.

We include simple illustrations and lots of examples, so you can see the power of an HSA and determine how you can potentially maximize your savings opportunity. The truth is that HSAs aren't complicated, but there are little tricks that can make a world of difference.

#1 Get lower health plan premiums

Enrolling in an HSA-qualified health plan often allows you to secure much lower monthly premiums compared to traditional Preferred Provider Organization (PPO) plans.

HSA eligibility requires enrollment in an HSA-qualified health plan, often called a "consumer choice" or "high-deductible" health plan. If you're not enrolled in one of these health plans, you can't make HSA contributions and take advantage of the associated tax-saving benefits.

Check your plan documents: You might find the savings on premiums alone can be thousands each year. That's less money out of your paycheck and more money in your pocket.

Here's an example for illustration.²

| Traditional Health Plan | HSA-Qualified Health Plan |

|---|---|

| $250 Monthly Premium | $125 Monthly Premium |

| $1,500 Annual HSA-qualified health plan savings | |

Be sure to read our article on high-deductible health plans for more information.

#2 Reduce your annual tax bill

HSA contributions are tax-deductible, meaning every dollar you contribute reduces your annual taxable income and lowers your overall tax burden.

Contributions to your HSA are tax deductible, which means every dollar you contribute can reduce your annual taxable income. If your employer offers an HSA, then typically you can sign up to make pre-tax payroll contributions. But even contributions you make on your own are tax-deductible.

You can always view the latest IRS contribution limits in our Open Enrollment center.

You won't pay federal income taxes, nor will you pay FICA payroll taxes. Most states also do not tax HSAs. Depending on where you live and your unique tax situation, that can translate into substantial tax savings on those HSA contributions.

Let's say your effective tax rate is 30% and you contribute $8,000 for the year. You could see $2,400 in tax savings, since that is $8,000 on which you will not pay any taxes at all.3

#3 Grab your employer HSA contribution

Many employers offer free seed contributions or matching funds directly to your Health Savings Account just for choosing an HSA-qualified health plan.

Your employer's potential HSA contributions could equal hundreds or thousands of dollars each year. Be sure to review your plan documents to see if an employer HSA contribution is available. Keep in mind that employer contributions count toward annual Internal Revenue Service (IRS) contribution limits.

Some employers offer $1,000 or more just for choosing an HSA. Some match your monthly contributions up to a certain amount, similar to a 401(k) match.

#4 Maximize your spending power

Because HSA contributions are tax deductible, you get to keep 100% of every dollar you contribute. That means when you use your HSA to pay for qualified medical expenses, you are stretching your dollars further.

In other words, your HSA gives you an instant boost on money to pay for thousands of everyday healthcare expenses, including doctor visits, dental care, prescriptions, over-the-counter medications, and more.

Want to learn more about ways to spend your HSA? Start with this list of 17 awesome ways.

#5 Create a healthcare emergency safety net

One of the biggest differences between a Flexible Spending Account (FSA) and an HSA is that unused FSA funds eventually expire and are forfeited back to your employer. By contrast, money in your HSA rolls over each year, every year, even if you change employers, health plans, or retire.

This enables you to save for unplanned, future medical expenses.

Most Americans aren't prepared for an unexpected $500 emergency medical bill. But HSA holders are 31% more likely to have reserves for just such an expense. Seventy-seven percent of HSA holders have $500 or more saved, compared to 59% of non-HSA holders, according to the Spring 2026 Healthcare Affordability Pulse.4

Think of your HSA as an extension of your emergency fund. The same way you keep extra savings for an unexpected home repair or car accident, your HSA lets you keep extra savings for a healthcare emergency.

Don't get caught by surprise.

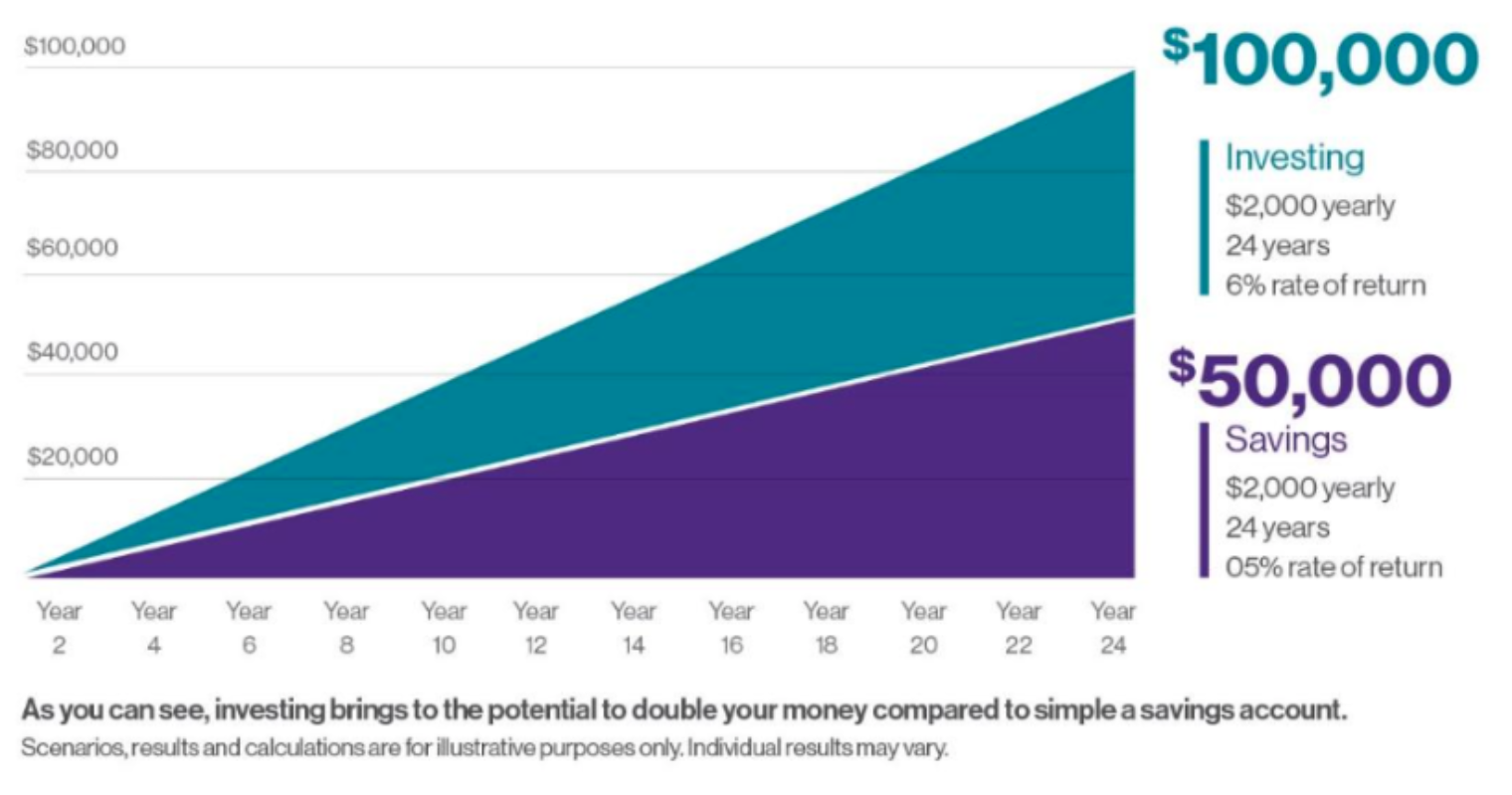

#6 Invest your HSA in low-cost mutual funds

You can invest your Health Savings Account balance in low-cost mutual funds to capitalize on compounding returns and potential tax-free account growth over time.5

HealthEquity offers a lineup of low-cost mutual funds, and options for self-directed or guided investing.

The potential growth of HSA investing compared to a low-yield savings account is substantial.6 For illustration, assume a $2,000 annual contribution and a 6% return each year for 24 years.

For context, the S&P 500 has delivered an average annual return of 10.5% since 1957, according to Investopedia.

#7 Save for healthcare expenses in retirement

When it comes to retirement, the 401(k) may be more well known. But your HSA can be one of the best accounts for saving for retirement. Not only can you invest your HSA and potentially capitalize on tax-free growth, but your HSA also provides tax-free distributions for qualified medical expenses.

A healthy couple retiring at age 65 needs an estimated $388,000 in savings to cover their remaining lifetime health expenses, according to the Milliman Retiree Health Cost Index.

That's why more Americans than ever are investing in their Health Savings Account (HSA) to build long-term retirement healthcare savings.

| HSA | 401(k) | |

|---|---|---|

| Assets | Investable | Investable |

| Contributions | Not taxed | FICA taxed |

| Earnings | Not taxed | Not taxed |

| Distribution for qualified medical expenses | Not taxed | Taxed (As ordinary income) |

| Distribution for non-qualified medical expenses | Taxed (As ordinary income after age 65) | Taxed (As ordinary income after age 59-1/2) |

| Required minimum distribution | Never | Yes (age 72) |

In addition, HSAs do not have required minimum distributions. Plus, members age 65 and older can take taxable HSA distributions for any expense—just like a 401(k). And, of course, distributions are always tax-free when used for qualified medical expenses.7

Considering how much you are likely to spend on healthcare in retirement, those advantages can translate into significant savings.

#8 Delay reimbursement to capitalize on tax-free account growth

The IRS does not require immediate reimbursement for medical expenses, allowing you to pay out of pocket, save your receipts, and let your HSA funds grow tax-free for years.

One thing that makes your HSA uniquely flexible is that the IRS does not stipulate a required reimbursement timeframe. This creates opportunity to effectively "bank" your receipts and save them to pay yourself back down the road.

How it works:

- Step 1: Pay for healthcare now out of pocket.

- Step 2: Save your receipt.

- Step 3: Let the money in your HSA grow.

- Step 4: Reimburse yourself whenever you want.

Delayed reimbursement allows you to compound any investment and interest earnings. Then, you can take money from your HSA whenever you need it, even if you wait 20 or 30 years.

The key is that you must save your receipts. If you get audited by the IRS, you will need to document past expenses, otherwise you could be subject to income tax and penalties.

#9 Gift health savings to your heirs

You can designate a beneficiary for your Health Savings Account, ensuring your remaining funds transfer to your loved ones after you pass away.

The IRS allows you to designate a beneficiary to your HSA, so in the event of death your account will transfer to whomever you designate.

When we say your HSA stays with you no matter what, we mean it!

You can roll over your HSA for the rest of your life and gift the money in the account to your heirs. In fact, right now you can log into your HealthEquity account and designate a beneficiary.

So, go ahead. Designate the beneficiary of your hard-earned health savings.

#10 Impress friends and family with your personal finance savvy

Sharing the triple-tax advantages of an HSA can help your friends and family improve their own healthcare affordability and personal finance strategies.

HSAs are popular, no doubt about it. But there are still too many Americans unfamiliar with HSAs and their power to build health savings.

Tell your friends and family about your HSA and its triple-tax advantage. They'll value your perspective. Plus, they'll be impressed with how much you know about personal finance.

You've taken the step toward connecting health and wealth. Now, let's encourage others to join the movement.

Have questions? Visit our Help Center.

Frequently Asked Questions

What happens to my HSA if I change jobs? Because you own your Health Savings Account, the funds roll over and stay with you even if you change employers, switch health plans, or retire. You never forfeit your unused balances.

What qualifies as a medical expense for an HSA? You can spend HSA funds on thousands of IRS-qualified medical expenses, ranging from doctor visits, copays, and deductibles to over-the-counter medications and vision care.

Can I withdraw HSA funds for non-medical expenses? Yes, but if you are under age 65, withdrawals for non-qualified expenses are taxed as ordinary income and subject to an additional penalty. After age 65, you can withdraw funds for any reason without penalty, though non-medical withdrawals are still taxed as ordinary income.8

HealthEquity does not provide legal, tax, or financial advice. Always consult a professional when making life-changing decisions.

1 HSAs are never taxed at a federal income tax level when used appropriately for qualified medical expenses. Also, most states recognize HSA funds as tax-deductible with very few exceptions. Please consult a tax advisor regarding your state's specific rules.

2 Scenarios, results and calculations are for illustrative purposes only. Individual results may vary.

3 Estimated savings are based on an assumed combined federal and state effective income tax rate of 30%. Actual savings will depend on your taxable income and tax status.

4 HealthEquity Healthcare Affordability Pulse, Spring 2026.

5 Investments are subject to risk, including the possible loss of the principal invested, and are not FDIC or NCUA insured, or guaranteed by HealthEquity, Inc. Investing through the HealthEquity investment platform is subject to the terms and conditions of the Health Savings Account Custodial Agreement and any applicable investment supplement. Investing may not be suitable for everyone and before making any investments, you should carefully consider the investment objectives, risks, charges and expenses of any mutual fund before investing. A prospectus and, if available, a summary prospectus containing this and other important information can be obtained by visiting the fund sponsor's website. Please read the prospectus carefully before investing.

6 Scenarios, results and calculations are for illustrative purposes only. Individual results may vary.

7 After age 65, if you withdraw funds for any purpose other than qualified medical expenses, you will be subject to income taxes. Funds withdrawn for qualified medical expenses will remain tax-free.